SPECIAL FOCUS: PATHWAYS FOR SUSTAINABLE HYDROGEN

A. STEINHUBL, Vice Chair of the Board, The Center for Houston’s Future, Houston, Texas

The global shift to decarbonization, earlier catalyzed by the Paris Accord and the related realization of the imperative to limit future global warming, has accelerated. The COVID-19 pandemic has raised awareness of the relationship between economic activity, energy consumption and the environment. The presently carbon-intensive energy system must be decarbonized to meet the dual challenges of expanding energy demand and producing cleaner energy. The potential for economic recovery stimulus through investment in clean energy infrastructure has been embraced by multiple regions and nations. The US is among them, upon the election of President Joe Biden and his stated priorities and initial actions to move toward a less carbon-intensive energy system.

These global and national trends overlay Texas energy transition imperatives, and perhaps surprisingly, the state’s new opportunities. An expanded hydrogen economy is one option among other, interrelated, low-carbon leadership opportunities that include increased application of carbon capture, use and storage (CCUS), expanded electrification and further penetration of renewable power.

Moreover, an expanded Texas H2 sector would leverage multiple aspects of existing energy system infrastructure and other Texas resources. Additionally, H2 system expansion would take advantage of the state’s significant labor, corporate, and academic institution capabilities, enabling the delivery of capital-intensive commodities to global customers both safely and cost efficiently.

The Center for Houston’s Future and the University of Houston, with support from other key collaborators, conducted assessments to identify opportunities for expanding clean H2 value chains in Texas and to develop a vision and roadmap to enter and expand new markets for H2. The institutions looked beyond the considerable existing H2 production and use in the Houston Gulf Coast region, which is predominantly used for oil refining and petrochemical feedstock. The purpose of this article is to summarize the outcomes of that work.

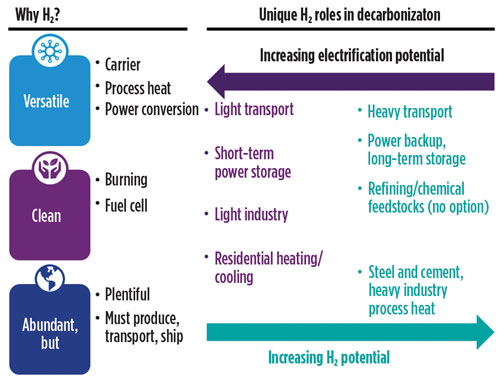

The push by many regions and nations to develop decarbonization plans has increased the focus on the unique and multiple potential roles of H2 in a low-carbon energy system (FIG. 1).

Fig. 1 Hydrogen’s unique advantages and critical roles in decarbonization.

Since the start of 2020, multiple regions have developed strategies to use H2 in achieving decarbonization goals, including the European Commission and several European countries (Germany, the Netherlands, Norway, Portugal, Spain and France).

Preeminent energy companies, including Shell, BP and Repsol, have also made low-carbon commitments and announced plans for H2 projects to help meet their commitments. Such plans help explain why substantial growth in the market for H2 gas and related equipment, such as electrolyzers and fuel cells, is projected by the Hydrogen Council at $2.5 T by 2050.

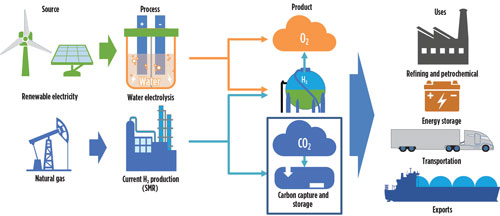

Today, most H2 is manufactured using natural gas (or in some regions, coal) to provide methane input for steam methane reforming (SMR). H2 is stripped in the process, creating CO2 as a byproduct. H2 produced in this manner is known as gray H2. When gray H2 production is coupled with CCUS, it is termed blue H2.

An alternative pathway to creating H2 is via electrolysis of water, splitting a water molecule into H2 and O2. When such electrolysis is powered with renewable energy, such as wind or solar, the H2 produced is known as green H2. FIG. 2 illustrates these two primary H2 pathways.

Fig. 2 Typical H2 production options and uses.

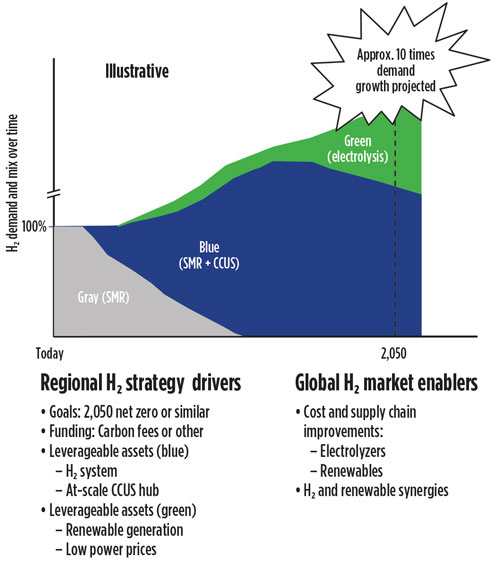

The preferred path, or combination of paths, to achieve the required rampant expansion in H2 will vary by region. Industrial areas with existing refining operations and petrochemicals production (e.g., the Netherlands, Germany and the U.S. Gulf Coast), which currently produce extensive H2 through SMR technology, will look to exploit their existing infrastructure to create blue H2. Less industrialized countries and those without indigenous fossil resources will likely either import H2 or seek to develop green H2 chains to the extent that renewable energy resources are available.

Emerging regional and country strategies, therefore, typically focus on the relative role and timing of two factors:

An illustration of such an H2 mix strategy, as well as the drivers for how such a strategy would be customized by region, are shown in FIG. 3.

Fig. 3 Strategy and drivers for a mixed H2 production system.

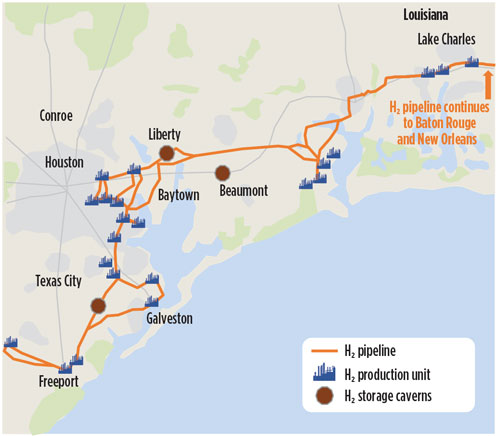

The Texas Gulf Coast area anchors the world’s leading H2 system, producing approximately one third of U.S. total H2 gas per year. The system encompasses an expansive network of 48 H2 production plants, more than 900 mi of H2 pipelines (more than half of the U.S. H2 pipelines and one third of H2 pipelines globally), as well as geologically unique and at-scale salt cavern storage (FIG. 4).

Fig. 4 Existing H2 system in the U.S. Gulf Coast region. Sources: H2Tools, USDOT–PHMSA, Air Liquide, Air Products, Praxair.

Today, this system primarily serves the U.S. Gulf Coast’s refining and petrochemical industry. By leveraging this system through coupling gray H2 production with CCUS, there is the potential to bring substantial volumes of H2 to new markets rapidly and at scale.

The eastern portion of the U.S. Gulf Coast H2 system overlays existing CCUS infrastructure—the Denbury system, which was developed to bring CO2 to recover oil reserves through enhanced oil recovery (EOR). Several large SMR facilities are proximate to the Denbury system and could be linked to it via pipeline to initiate the move from gray to blue H2. Over time, a CCUS system could be expanded, tapping into additional active and depleted reservoirs throughout the U.S. Gulf Coast both onshore and offshore. This CCUS system potentially could be expanded into the Permian basin with its vast extent of active and depleted reservoirs.

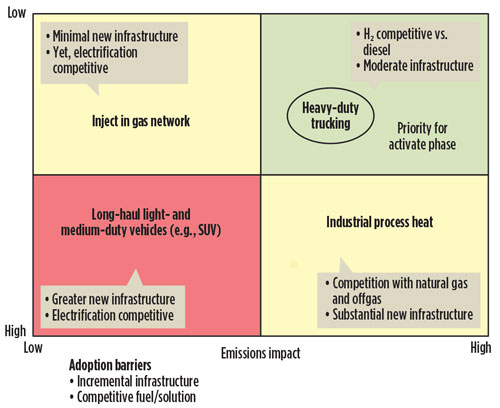

There is a need to match the development of clean H2 with an end-use market. Multiple market applications exist for H2 beyond its existing primary uses in oil refining and as petrochemical feedstock. Here, new H2 market opportunities are prioritized based on the extent of new infrastructure needed, the competitiveness of H2 over existing fuels or other clean alternatives (e.g., electrification) and the relative emissions reduction (FIG. 5).

Fig. 5 Initial prioritization of blue H2 markets.

It was concluded that heavy trucking should be an initial priority to investigate in Texas. Trucking requires limited new infrastructure to utilize H2 as a fuel, and H2 fuel competes with relatively expensive and relatively higher-emitting diesel fuel. The advantages of H2 fuel cell power in this application are many: low weight, fast refueling, high range and relatively low new infrastructure costs. Additionally, the speed of refueling, as well as range and torque requirements, favor H2 over batteries in the heavy trucking application. Emissions still would be lower than diesel, even if the H2 fuel was gray H2. As gray H2 is paired with CCUS to create blue H2, the emissions benefit of using H2 fuel increases.

Heavy trucking was validated to be particularly attractive as an initial new market by modeling H2 economics relative to diesel in specific trucking corridors in Texas. Several high-concentration trucking markets involve the Houston and Houston port areas, Dallas (which is a regional distribution hub) and San Antonio (which ties into shipping from Mexico). Tapping high-density corridors minimizes the infrastructure required to achieve meaningful scale regionally, thereby improving the economics of market entry and expansion.

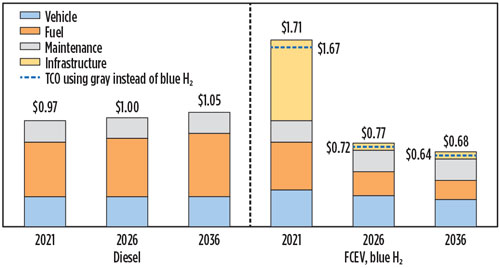

FIG. 6 illustrates the potential economics of the Interstate-45 (I-45) highway corridor connecting Houston with Dallas. A DOE-funded, low-emissions planning study is underway for this corridor by the North Texas Council of Governments. As with analogous markets, such as the Port of Los Angeles, economics are favorable for the I-45 corridor at scale vs. diesel fuel. Coupling this potential with the facts that vehicle manufacturers such as Nikola, Toyota and Hyundai are developing and piloting the manufacture of H2 trucks, and shippers are increasingly seeking to curb their emissions, there is promise that this could be an early new H2 market in Texas.

Fig. 6 Total cost of ownership for diesel vs. H2 heavy-duty trucks on the I-45 Houston–Dallas corridor, $MM/truck. Sources: ANL, HDSRAM, ICCT, EIA.

Adoption of H2 as a fuel at the Port of Los Angeles and other geographies has been catalyzed by incentives to update truck fleets to lower-emissions fuels and to build infrastructure. Incentive requirements would be less in these scenarios, given the Texas region’s present H2 production and dense heavy-trucking patterns. Therefore, it was concluded that demonstration pilots to produce H2 to power fuel cells can be set up over the next few years, taking advantage of the confluence of the existing low-cost, high-scale U.S. Gulf Coast H2 system to supply proximate heavy-duty trucking corridor demand.

As outlined in the previous sections, clear opportunities exist to bring gray and blue H2 to market at scale quickly in Texas, and potentially for export to other regions. Doing so would accelerate decarbonization efforts while green H2 value chains—requiring additional renewable power and electrolyzer capacity—are developed.

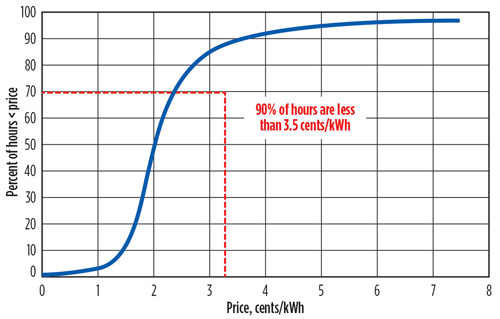

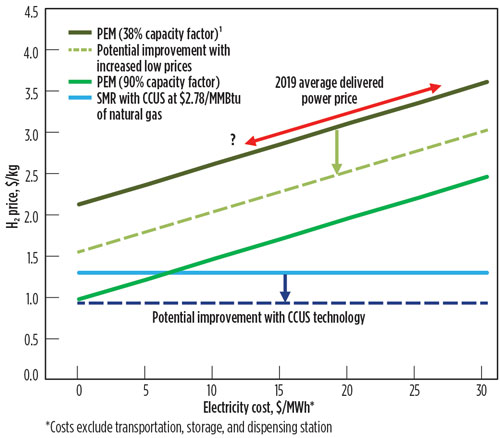

The region and the state hold significant advantages to incubate green H2, which is produced via splitting a water molecule through electrolysis to create zero-emissions H2. An important advantage, given the significant power consumption requirements for electrolysis, is that the Texas power market includes many hours of low-priced power due to a generation mix heavy in windpower (Texas is the number-one windpower-producing state), as well as a rapidly growing solar fleet. FIG. 7 demonstrates the effects of this extensive renewable power base on the availability of very low-price power hours. Given the high-power consumption presently required for the production of H2 via hydrolysis, low power prices create an advantage.

Fig. 7 Houston wholesale power price duration curve. Source: ERCOT.

H2 produced during low-cost hours can serve as long-duration H2 storage (i.e., H2 serves as a mechanism to store energy during periods of high renewable power input such as sunny days or weeks and provides power during periods of shortage such as cloudy days or days with no wind).

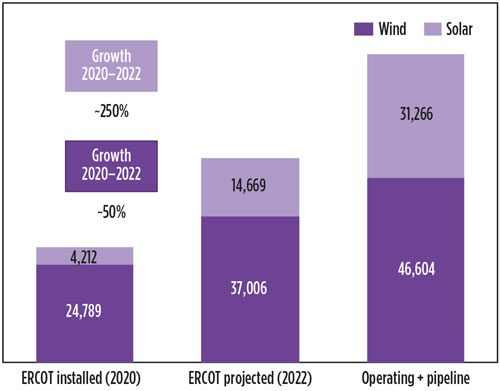

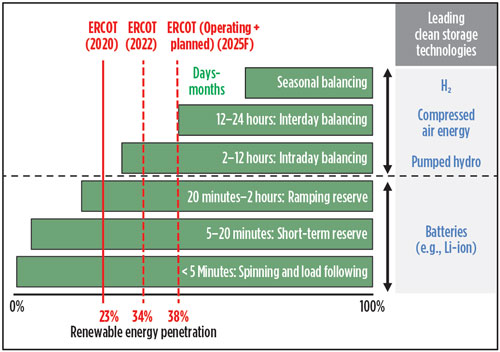

Moreover, coupling H2 salt cavern storage, uniquely prolific in the Houston Gulf Coast area, with low-priced power creates the further opportunity to use H2 in (even greater duration) seasonal storage (i.e., H2 serves as a mechanism to store energy during periods of low-cost power in the winter, to be used during peak power prices in the summer). FIG. 8 and FIG. 9 illustrate the expected growth in Texas renewable power and additional low-price hours, as well as the synergistic role of H2 as a storage medium as power intermittency issues rise with more renewable power on the Texas grid.

Fig. 8 ERCOT installed and potential wind and solar capacity, MW. Source: ERCOT.

Fig. 9 Energy storage requirements vs. renewable energy penetration levels. Source: ERCOT.

Four key initiatives are recommended to activate blue and green H2 opportunities in the Texas region:

These activation initiatives will require approximately $565 MM over 10 yr, appropriate policy changes and public funding to help defray the costs of new infrastructure buildout, equipment changeout and facilitating permitting. Applying CCUS to produce blue H2 as a fuel could be incentivized both by CCUS policy (e.g., the federal 45Q tax credit, possibly with enhancements), as well as by a potential clean fuels incentive. Other incentives and policy changes will be needed over time to further develop new chains and markets for H2.

Potential opportunities exist to expand blue and green H2 production in the region, as clean H2 demand continues a sharp increase through 2050. Additional market uses beyond heavy trucking include industrial process heat, electric power production and building heating—all of which exist in large quantity in the region. As H2 system costs continue to improve, potentially accelerated through policy incentives and support, the potential for additional market opportunities grows as the comparative economics of H2 vs. the existing fuel or energy solution improves, and infrastructure costs are amortized over increasing scale.

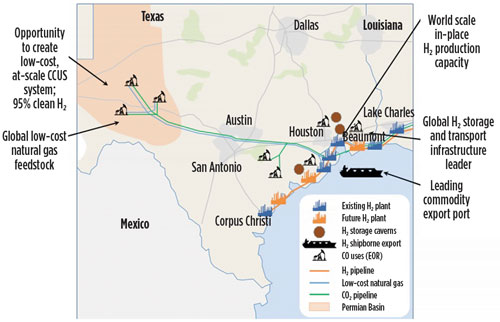

Many markets, domestically and globally, will need more H2 than they can produce over the next decade to meet decarbonization goals. Some markets, domestic and international, will need to import H2 to meet demand. A strong case exists for the Houston Gulf Coast to become a global blue H2 exporter with its world-scale, in-place H2 production capacity; low-cost natural gas feedstock; opportunity to create a low-cost, at-scale CCUS system; and global H2 storage and transport infrastructure.

For example, a promising, early blue H2 opportunity for Houston could be exporting to California to take advantage of the latter state’s Low Carbon Fuel Standard incentive. A blue H2 system, anchored in the Texas Gulf Coast area, could expand to become a major H2 exporter, leveraging its low cost, existing scale, and advantaged pipeline and shipping positions. This could be a mid-term strategy to accelerate at-scale volumes of clean H2 to domestic and global markets. Initial export markets may include domestic trucking markets beyond California or international markets, such as the Netherlands, Germany or Japan, which have regional supply projections short of demand requirements.

Capturing full value from new H2 market opportunities (assuming incentives for clean H2) will likely require leveraging the existing SMR system and, potentially, creating new methane-based H2 production paired with CCUS.

New blue H2 production with even lower net emissions could be realized through constructing plants with alternative technologies, such as autothermal reforming (ATR), as is planned in the Netherlands’ Port of Rotterdam and UK Humber areas, and/or incorporating biomass feedstocks.

Building out the required CCUS system would likely occur in phases:

An expanded role is envisioned for green H2 as renewable power penetration increases, as electrolysis costs and production efficiencies improve, and as policy and market trends evolve. Green H2 could be readily integrated into the existing Gulf Coast storage, shipping and other infrastructure systems.

Rollout of Texas’ H2 plans. The outlook for a “rollout phase” is uncertain and depends on multiple forces that will significantly shape the demand, pace and source of H2 in decarbonization. For example, public policy changes, investor preferences, renewables and electrolysis technology and cost trends could accelerate green H2 to playing a larger role, sooner.

On the other hand, decarbonization goals and timing, CCUS technology and uptake trends, and public carbon policy could extend the role of blue H2 in meeting rising global decarbonization needs. At present, the estimated H2 cost of coupling SMR production with CCUS is significantly cheaper than green H2 in the Houston region due to existing SMR H2 infrastructure, low natural gas feedstock costs, and the opportunity to leverage and extend existing CCUS infrastructure (FIG. 10).

Fig. 10 Case for Houston as a global blue H2 exporter.

Gray and blue H2 is also widely available at present, while green H2 is not. However, electrolysis investment costs and efficiency are projected to improve significantly as manufacturing increases and technology advances. These factors, along with the previously mentioned renewable power availability, price reductions and other forces, could spur additional green H2 at lower cost (FIG. 11).

Fig. 11 Current blue and green H2 production costs in Houston. Source: S&P Platts.

A key decarbonization opportunity is the U.S. Gulf Coast region’s vast industrial sector, which comprises approximately 30% of U.S. refining capacity and more than 40% of U.S. petrochemical capacity.

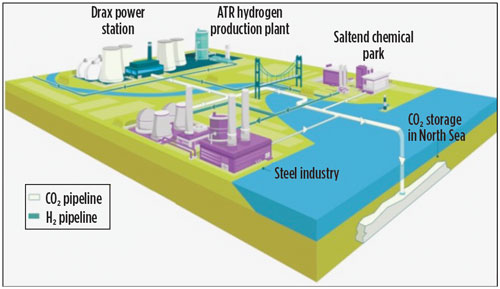

The region’s industrial sector accounts for 40% of Texas’ industrial emissions, totaling 65 metric MMtpy. Other regions, such as Rotterdam in the Netherlands and Humber in the UK (FIG. 12), have developed plans to use H2 to decarbonize industrial process heat and power by burning H2 instead of fossil fuels. Adapting infrastructure to burn H2 requires substantial investment. The Netherlands and the UK have instituted carbon taxes, along with public funding, to support private investment.

Fig. 12 Schematic of Humber, UK industrial area. Source: Equinor.

The Texas region has an opportunity to emerge as a leading global H2 hub. An emerging view across many industrialized regions with H2 plans suggests a larger role for blue H2 through the medium term—now through the 2030s or 2040s, while at the same time accelerating green H2 development. The timing and extent of low-carbon policy could change overall H2 demand and the mix of blue H2 vs. green H2.

Cost-competitive green H2 with scale volume potential is anticipated to emerge in the 2030s and beyond as electrolysis costs and technology improve, as fuel-cost manufacturing and scale economies improve, and as more ubiquitous and low-cost renewable power is available.

The substantial demand for clean H2 in the near and medium term, favoring blue H2, followed by improving and expanding green H2 opportunities, presents a unique opportunity for the Texas region. Leveraging its world-class H2 infrastructure, personnel and corporate assets, Texas can globalize its H2 leadership and emerge as a leading global H2 hub, driving lower emissions and bridging between old and new energy systems as a path to continue energy leadership, economic expansion and job growth (FIG. 12).

To tap this longer-term potential—as blue and green H2 technologies and costs advance and macro-policy goals regarding decarbonization take shape—additional and adaptive policies and funding mechanisms will be required. Early establishment of these policies would help the Texas region keep pace with decarbonization initiatives in other parts of the world.

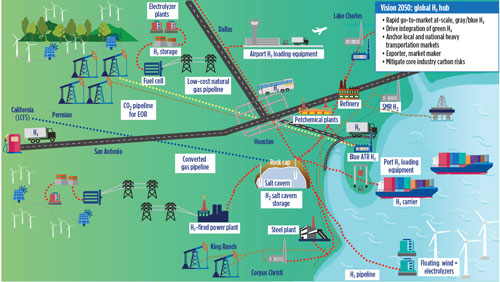

Research commissioned by The Center for Houston’s Future and the University of Houston shows that Texas has a significant opportunity to both reduce its carbon emissions from existing H2 production while creating new market opportunities from the energy transition (FIG. 13).

Fig. 13 The 2050 vision for a Texas H2 economy.

Furthermore, the opportunity exists to globalize Texas H2 leadership. There is no question that the energy system is changing; the issue is whether Texas will transition rapidly enough to capture its potential. This report shows the path forward.

ANDY STEINHUBL serves as Vice Chair of the Board and sits on the Executive and Nominating Committees of the Center for Houston’s Future. He recently retired with more than 35 yr of energy experience, having launched and led KPMG’s U.S. Energy and Chemicals strategy group. Prior to joining KPMG, he worked for Booz & Co., where he served as the Houston office’s Managing Partner and in a variety of North American and global energy sector leadership roles. He began his career at ExxonMobil. At present, Mr. Steinhubl is collaborating with the Center for Houston’s Future on a variety of projects regarding Houston’s role in the energy transition, including the role of H2 in the decarbonization of Houston’s energy system.

Mr. Steinhubl earned a BS degree in chemical engineering at Purdue University and an MBA degree from Stanford University’s Graduate School of Business.

Fig. 1. Hydrogen’s unique advantages and critical roles in decarbonization.

Fig. 2. Typical H2 production options and uses.

Fig. 3. Strategy and drivers for a mixed H2 production system.

Fig. 4. Existing H2 system in the U.S. Gulf Coast region. Sources: H2Tools, USDOT–PHMSA, Air Liquide, Air Products, Praxair.

Fig. 5. Initial prioritization of blue H2 markets.

Fig. 6. Total cost of ownership for diesel vs. H2 heavy-duty trucks on the I-45 Houston–Dallas corridor, $MM/truck. Sources: ANL, HDSRAM, ICCT, EIA.

Fig. 7. Houston wholesale power price duration curve. Source: ERCOT.

Fig. 8. ERCOT installed and potential wind and solar capacity, MW. Source: ERCOT.

Fig. 9. Energy storage requirements vs. renewable energy penetration levels. Source: ERCOT.

Fig. 10. Case for Houston as a global blue H2 exporter.

Fig. 11. Current blue and green H2 production costs in Houston. Source: S&P Platts.

Fig. 12. Schematic of Humber, UK industrial area. Source: Equinor.

Fig. 13. The 2050 vision for a Texas H2 economy.